At MSE we know how daunting buying your first home can be, and the already big hurdles that come with homebuying have only been raised higher by the disruption caused by coronavirus and the resultant lockdown.

In this blog, we (MSE Katie, Kit, Molly, Holly and Becky) – who are all at various stages of the homebuying process – have put our heads together to lend you (see what we did there?) some of our hard-earned knowledge about getting on the first rung of the property ladder during a pandemic. We hope everything here helps you decide whether buying a home is right for you now, and, if it is, how best to avoid heartbreak and frustration.

Even with (dare we say it ourselves) above-average expertise and insider knowledge on our side, the market has been vastly different compared to normal times. Here’s everything we’ve learned along the way… and stuff we wish somebody else had told us too!

1. Before you start house-hunting, CHECK if you can realistically get a mortgage – it’s a whole new world for homebuyers out there

In normal times, first-time buyers usually take their first steps on to the property ladder with a smallish deposit, usually 10%, or sometimes even 5%. But as the pandemic’s put pressure on banks, the mortgage market has shrunk massively, with our much-needed 90% and 95% mortgages in short supply. It’s meant significantly fewer mortgage options – if any – for most first-time buyers with lower deposits.

It’s worth considering what property value you could afford if your deposit had to now be worth 15% or even 20% of its price. If you could be happy in what would likely be a smaller property, or in a different area, it’s worth considering as this will likely give you more mortgage options to choose from.

MSE Katie experience a lack of willing mortgage lenders:

” When we applied for our mortgage, there was one single lender who was offering 90% loan-to-value. Living in commuting distance of MSE Towers in London meant that we couldn’t stretch to a bigger deposit and still have the kind of property we wanted. Sure enough, a week after we applied, that lender withdrew its 90% mortgages from the market – we were so lucky to get in before.”

A good place to start is our Mortgage Best-Buys tool, which will give you an initial look at the market – and show you if there are actually any products available for your situation.

Remember. A good mortgage broker can be worth their weight in gold to help here too.

As the mortgage market moves so quickly in this pandemic, a mortgage broker will guide you through all the options and the lending process, which is especially helpful for a first-timer. They have access to the latest information about deals you might be able to get and how much you can borrow – plus they can help you plan for the future if it’s just not possible for you to get a mortgage right now.

For many brokers, you don’t have to pay a fee and you can get an initial assessment without committing – though make sure you ask them about their fees upfront just in case. While some brokers do charge, many make their money on commission from your lender once they arrange a mortgage for you.

2. Get a mortgage agreement in principle and reduce the risk of being let down later

Because the pandemic has left fewer options for first-time buyers, your word alone won’t be enough to prove to a seller you’ll get a mortgage. So it’s wise to get a mortgage agreement in principle (AIP) from a lender – in fact, many estate agents and sellers won’t consider you a serious buyer without one. It at least gives some indication that a lender will lend to you (though remember, an AIP is not binding).

MSE Kit found this when he was looking at properties:

” The seller of the property I am buying wouldn’t even allow viewings without an agreement in principle – so it’s a good job we got one when we did!”

MSE Katie added:

” Having a mortgage agreement in principle ready to go not only helped me to clinch the offer with the seller, it also meant it was much quicker and easier to start the ball rolling with a formal mortgage application. It also saved me a lot of heartache – other properties I missed out on are now back on the market, showing just how likely it is that buyers are struggling to get the mortgage they need.”

3. If you’ve been furloughed or work in an at-risk sector, you’ll need proof, ie, a letter, to show that your job is safe

If you’ve returned to work from furlough, and have at some point received 80% of your normal salary, lenders will need to be certain of your full income going forward. Some will ask you to get a letter from your company which states that you’ve been brought back from furlough, on what date, and crucially, what your normal salary will be from now on. This will likely be mandatory in order for the lender to approve your loan, especially if your most recent bank statements show reduced income.

MSE Katie had to get one of these as part of her and her partner’s mortgage application:

” My partner was on furlough for two months during the pandemic. Our mortgage lender needed to see copies of our bank statements – so he was asked to provide his return-from-furlough letter to prove his lower salary payment was not usual.

The original letter from his employer didn’t include his salary – the most important part. We were lucky, he works for a large company and it was sorted within hours. But for some, this could take days or weeks to request from HR. This turned out to be a really important document, so it’s easier to ask for it before you even apply.”

This has another benefit while house-hunting – having documentation like this proves to the estate agent that your job is no longer at risk and you are less likely to be turned down for a mortgage.

If you’re working in an industry that’s more unstable in the pandemic, like the travel industry, it’s best to be upfront and tell your mortgage broker this, in case there are any restrictions on lending. This will save you being let down further along in the process and will help the broker to give you a true picture of the mortgages you may be able to get.

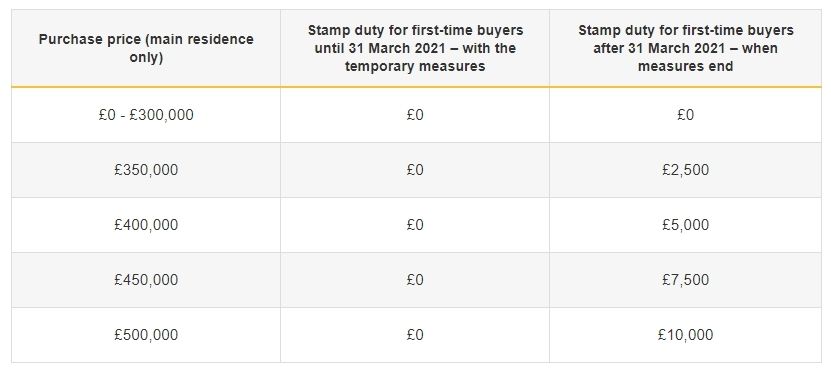

4. Don’t rush just to beat the coronavirus stamp duty holiday – most first-time buyers don’t pay stamp duty anyway

There’s been a lot of talk about the stamp duty threshold being increased to £500,000, and this has seemingly contributed to a mini property boom – according to property website Rightmove, more than £37 billion worth of property sales were agreed in July, the busiest month for 10 years.

But while this change is great, don’t let this be THE reason you decide to buy, or let it unnecessarily rush you if you are in two minds. That’s because most first-time buyers don’t pay stamp duty anyway.

Under normal stamp duty rates (which kick back in from April 2021), first-time buyers pay zero stamp duty on the first £300,000 of a property’s sale value (as shown in the table below). They then pay 5% of the portion from £300,001 to £500,000. After that, normal rates apply.

According to Zoopla, the average cost of a home for a first-time buyer is £220,000 – so the majority of us are buying well within that tax-free limit.