House prices have fallen for the third month in a row in May, new research has revealed

Property prices have fallen for the third month in a row in May as coronavirus stalled activity in the market, a housing report shows.

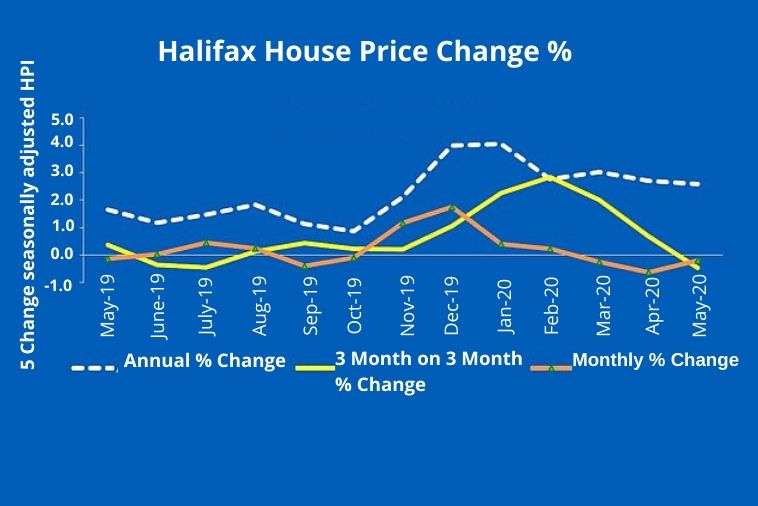

However, the decline has been modest, with just a 0.2 per cent monthly downturn in values, according to the Halifax index.

The fall took the average house price in Britain to £237,808, the lender said – this is 2.6 per cent higher when compared with the same time a year ago.

Russell Galley, managing director at Halifax, says calculating the average house price ‘remains challenging’ with increased volatility to be expected, thanks to a limited number of transactions to base data on.

He adds: ‘This is the third successive monthly fall, though more modest than in April, and reflects a continued loss of momentum following what was a strong start to the year.’

The property market has been affected by the lockdown as estate agents were unable to physically show potential buyers around homes and instead rely on virtual viewings.

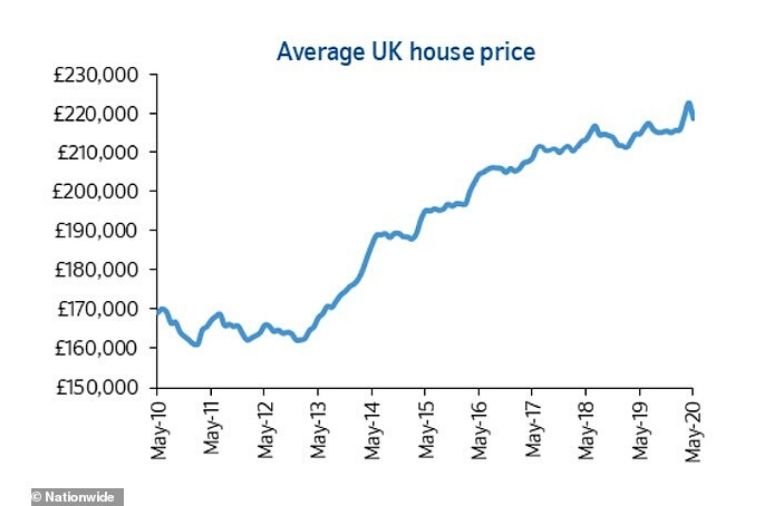

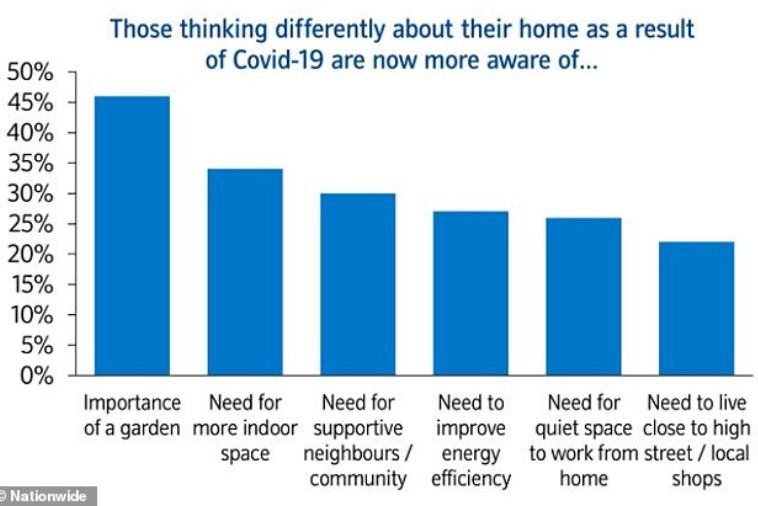

Halifax’s research differs to that of Nationwide’s house price index released earlier this week that said property values fell by 1.7 per cent month-on-month – or more than £4,000 – in May.

Nationwide claimed this was the biggest monthly fall in property values in 11 years.

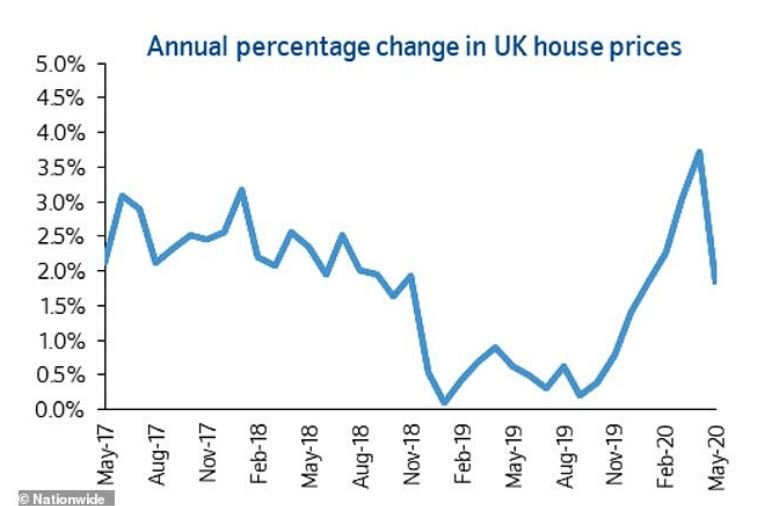

However, according to Halifax’s index, the average month-on-month price fall in May was just £506.

Jeremy Leaf, north London estate agent and a former RICS residential chairman, said: ‘Unlike the rather gloomy Nationwide figures from a few days ago, Halifax demonstrates a more hopeful picture for the market, even though prices have fallen for three successive months while emerging from the eye of the Covid storm.